5 Critical Expense Tracking Mistakes That Are Sabotaging Your Financial Goals

Sarah Mitchell

19 March 2026

5 Critical Expense Tracking Mistakes That Are Sabotaging Your Financial Goals

Introduction

You’ve downloaded the apps, set up your spreadsheets, and committed to tracking every penny. Yet somehow, your financial goals still feel impossibly out of reach. If this sounds familiar, you’re not alone. Over 73% of Americans struggle with budgeting despite having access to more financial tools than ever before.

The problem isn’t a lack of technology or willpower—it’s the fundamental mistakes in how we approach expense tracking. These seemingly innocent errors compound over time, creating blind spots that sabotage even the most well-intentioned financial plans.

In this comprehensive guide, we’ll uncover the five most damaging expense tracking mistakes that are quietly derailing your financial success. More importantly, you’ll learn practical strategies to fix these issues and finally make meaningful progress toward your financial goals.

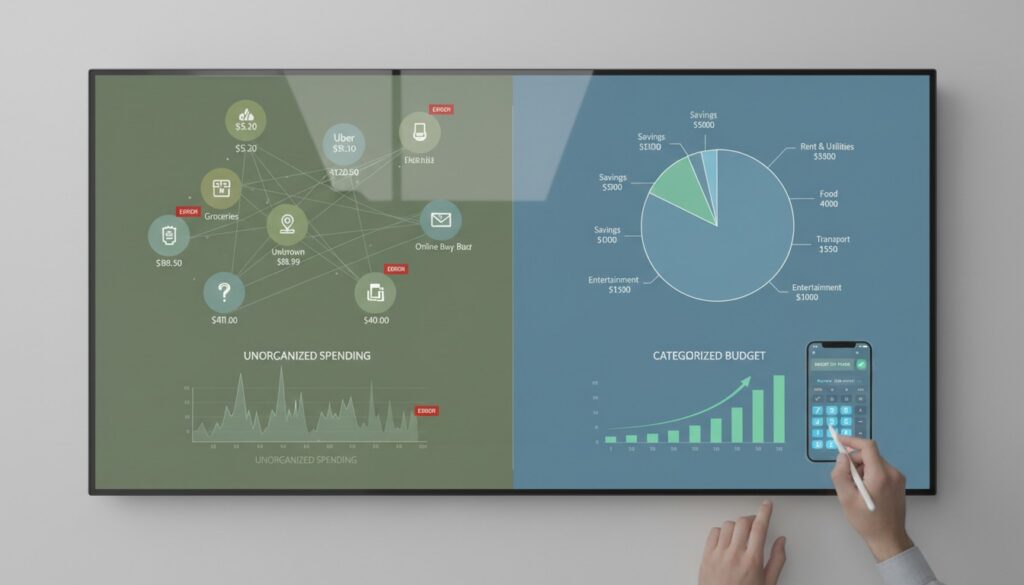

Mistake #1: Tracking Expenses Without Categorizing Them Properly

The Problem: Generic Expense Categories

Most people start expense tracking with broad categories like “Food,” “Entertainment,” and “Shopping.” While this seems logical, it creates a dangerous lack of specificity that prevents you from identifying spending patterns and making informed decisions.

Consider Sarah, a marketing professional who tracked $800 monthly in “Food” expenses. She assumed she was spending too much on restaurants, so she started cooking more at home. Despite her efforts, the food budget remained unchanged. The real culprit? $300 monthly on premium coffee and workplace lunches—expenses that required different solutions than dinner spending.

The Solution: Implement Granular Categorization

Create specific subcategories that reflect your actual spending patterns:

- Food: Groceries, Restaurants, Coffee/Beverages, Work Lunches, Delivery

- Transportation: Gas, Public Transit, Rideshare, Parking, Maintenance

- Entertainment: Streaming Services, Movies, Concerts, Hobbies, Books

- Shopping: Clothing, Electronics, Home Goods, Personal Care, Gifts

- Primary categories for broad budgeting

- Tags or subcategories for detailed analysis

- Memory gaps leading to forgotten expenses

- Emotional distance from spending decisions

- Delayed awareness of budget overruns

- Reduced accountability for impulse purchases

- Fresh memory of all transactions

- Immediate awareness of spending patterns

- Stronger psychological connection to spending decisions

- Early warning system for budget overruns

- Set a recurring calendar reminder

- Gather all receipts and check bank statements

- Review and categorize all expenses from the past week

- Analyze spending patterns and adjust upcoming week’s budget

- Bank account linking for automatic transaction imports

- Receipt scanning apps for instant categorization

- Spending alerts for real-time budget monitoring

- Weekly summary emails to maintain awareness

- Fall below our mental spending threshold

- Compound significantly over time

- Often continue after their usefulness expires

- Create budget “leaks” that are hard to identify

- Daily coffee: $4.50 × 22 workdays = $99/month

- Unused gym membership: $35/month

- Premium streaming services (3): $45/month

- Mobile app subscriptions: $25/month

- Total: $204/month or $2,448/year

- Review 3 months of bank and credit card statements

- Check your email for subscription confirmations

- Use apps like Truebill or Honey to identify recurring charges

- List every subscription, regardless of amount

- When did I last use this service?

- Does this provide ongoing value?

- Could I achieve the same result for less money?

- Would I sign up for this today at this price?

- Schedule recurring calendar reminders

- Track subscription start dates and free trial endings

- Monitor usage through service analytics when available

- Set spending limits for new subscription additions

- Phantom savings that don’t actually exist

- Unaccounted expenses that derail budgets

- False confidence in financial progress

- Repeated budget failures without understanding why

- Forgotten cash purchases (ATM withdrawals not tracked)

- Automatic payments not recorded in expense trackers

- Bank fees and interest charges overlooked

- Pending transactions that clear later

- Shared expenses on joint accounts

- Download statements from all accounts (checking, savings, credit cards)

- Export expense data from your tracking app or spreadsheet

- Compare total expenses between your tracker and bank records

- Identify discrepancies and investigate each one

- Update categories for any misclassified expenses

- [ ] All bank transactions have corresponding tracker entries

- [ ] All tracker entries match actual bank charges

- [ ] Cash withdrawals are accounted for with specific expense records

- [ ] Automatic payments are properly categorized

- [ ] Bank fees and interest charges are included

- [ ] Shared account expenses are proportionally allocated

- Mint: Free comprehensive tracking with bank integration

- YNAB (You Need A Budget): Paid service with robust reconciliation features

- Personal Capital: Investment-focused with expense tracking capabilities

- Repeated spending mistakes without learning

- Stagnant financial progress despite detailed records

- Frustration and abandonment of tracking systems

- Missed opportunities for significant savings

- Time-based patterns: Higher spending on weekends or specific months

- Emotional triggers: Stress spending or celebration purchases

- Location patterns: Expensive habits in certain places

- Category trends: Gradual increases in specific expense areas

- Calculate variance percentages for each category

- Identify seasonal fluctuations that affect planning

- Recognize lifestyle inflation in specific areas

- Spot impulse spending triggers

- Subscription consolidation opportunities

- Bulk purchase advantages for frequently bought items

- Timing strategies for major purchases

- Alternative solutions for expensive habits

- Spending limits for problematic categories

- Waiting periods before non-essential purchases

- Alternative activities to replace expensive habits

- Accountability systems for challenging areas

- Compare current month spending to budget

- Identify top 3 overspending categories

- Note any unusual or unexpected expenses

- Calculate remaining budget for each category

- Analyze 3-month spending trends

- Calculate cost-per-use for major purchases

- Identify seasonal patterns affecting budget

- Plan behavioral adjustments for next month

- Dining out: Plan meals and prep ingredients

- Entertainment: Find free or low-cost alternatives

- Shopping: Implement a “one in, one out” policy

- Generic categorization that hides spending patterns

- Inconsistent tracking that breaks the feedback loop

- Ignored small expenses that accumulate significantly

- Lack of reconciliation that creates false confidence

- Analysis paralysis that prevents meaningful change

Pro Tip: Review your last three months of expenses to identify your unique spending patterns before creating categories.

Advanced Categorization Strategy

Implement a dual-layer system:

This approach allows you to maintain simple budget oversight while gaining granular insights when needed.

Mistake #2: Inconsistent Tracking Frequency and Timing

The Problem: Sporadic Recording Habits

The most common expense tracking failure isn’t using the wrong app or method—it’s inconsistent recording. Many people start strong, tracking expenses daily for a week or two, then gradually slip into weekly or monthly updates. This inconsistency creates several critical problems:

The Impact of Delayed Tracking

Research shows that people who track expenses within 24 hours of spending are 40% more likely to stay within budget compared to those who update weekly. The psychological connection between spending and recording is crucial for developing better financial habits.

The Solution: Establish a Sustainable Tracking Rhythm

#### Daily Micro-Tracking (Recommended)

Spend 2-3 minutes each evening recording the day’s expenses. This approach offers:

If daily tracking feels overwhelming, commit to weekly sessions:

Automation Strategies

Leverage technology to reduce manual effort:

Mistake #3: Ignoring Small, Recurring Expenses

The Problem: Death by a Thousand Cuts

While you carefully track major purchases like rent and car payments, those seemingly insignificant recurring charges are quietly draining your budget. The average American has 12-15 active subscriptions, spending over $200 monthly on services they barely use.

These “micro-expenses” are particularly dangerous because they:

Real-World Impact Analysis

Let’s examine how small expenses accumulate:

The Solution: Conduct a Subscription Audit

#### Step 1: Comprehensive Discovery

For each subscription, ask:

#### Step 3: Strategic Elimination

Cancel immediately: Services unused in the past 30 days

Downgrade: Premium features you don’t actively use

Consolidate: Overlapping services (multiple streaming platforms)

Negotiate: Annual plans for frequently used services

Ongoing Maintenance System

Establish a quarterly subscription review:

Mistake #4: Not Reconciling Tracked Expenses with Bank Statements

The Problem: Living in a Fantasy Budget

Many expense trackers create detailed budgets and diligently record expenses, but never verify their tracking accuracy against actual bank statements. This creates a dangerous disconnect between perceived and real spending, leading to:

Common Reconciliation Gaps

Typical discrepancies include:

The Solution: Monthly Reconciliation Process

#### Week 1 of Each Month: Full Account Review

Advanced Reconciliation Techniques

#### The “Zero-Based” Approach

Your tracked expenses + savings + debt payments should equal your total income minus taxes. Any discrepancy indicates missing expenses or income.

#### Technology Integration

Use tools that automatically sync with bank accounts:

Remember: The goal isn’t perfect tracking—it’s accurate awareness of your actual spending patterns.

Mistake #5: Failing to Analyze Spending Patterns and Adjust Behavior

The Problem: Tracking Without Learning

The most sophisticated expense tracking system is worthless if you never analyze the data to identify patterns and make behavioral changes. Many people become obsessed with the mechanics of tracking while ignoring the insights their data provides.

This “tracking treadmill” leads to:

The Analysis Framework: The SPOT Method

#### S – Spending Patterns

Identify recurring themes in your expenses:

#### P – Problem Areas

Highlight categories where you consistently exceed budget:

#### O – Opportunities

Discover potential savings and optimization areas:

#### T – Tactical Changes

Implement specific, measurable behavioral adjustments:

Monthly Analysis Routine

#### Week 3 of Each Month: Deep Dive Review

15-Minute Quick Analysis:

45-Minute Comprehensive Review:

Behavioral Change Strategies

#### The “24-Hour Rule”

For non-essential purchases over $50, wait 24 hours before buying. This simple delay reduces impulse spending by up to 60%.

#### Category Challenges

Choose one overspending category monthly and implement specific reduction strategies:

Conclusion

Expense tracking isn’t just about recording numbers—it’s about creating awareness, identifying patterns, and driving behavioral change. The five mistakes we’ve covered represent the most common barriers between good intentions and financial success:

The path to financial stability isn’t about earning more money or finding the perfect app. It’s about understanding where your money goes and making intentional decisions about where you want it to go instead.

Take Action Today

Don’t let these insights become just another article you read and forget. Choose one mistake from this list that resonates most with your current situation and commit to fixing it this week.

Start small, but start now. Your future financial self will thank you for taking action today rather than waiting for the “perfect” moment that never comes.

Which of these five mistakes is currently sabotaging your financial goals? Share your biggest challenge in the comments below, and let’s work together to create accountability for positive change.